Ryan Lynch

Ryan Lynch

The tried-and-true playbook of CPG powerhouses like P&G, Anheuser Busch, and General Mills worked for decades, but many of these blue-chip brands are now struggling. While the pandemic didn’t help, in most cases, it simply accelerated trends that there were already in progress.

The tried-and-true playbook of CPG powerhouses like P&G, Anheuser Busch, and General Mills worked for decades, but many of these blue-chip brands are now struggling. While the pandemic didn’t help, in most cases, it simply accelerated trends that there were already in progress.

A recent McKinsey article walked through the traditional five-part model and analyzed why it is no longer effective. The steps in the CPG value creation model came into being after WWII and have barely changed since. They are:

- Building mass-market brands and innovating when consumer loyalty was stable

- Leveraging grocer/retail partnerships to "grow as they grew"

- Winning in developing markets. As incomes rose, so did the purchase of your products

- Taking cost out through centralization/operational excellence

- Acquiring more brands and driving them across your grocery/retail/developing markets to scale

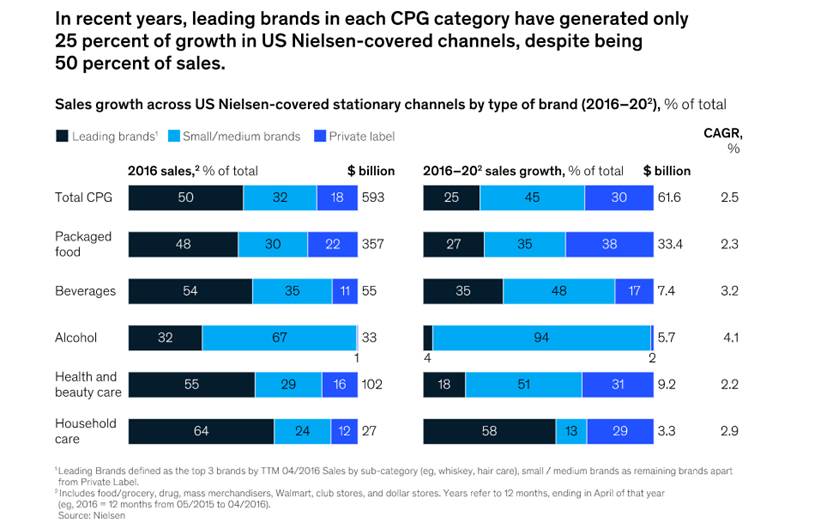

This playbook was highly successful for decades. With the advent of the internet and more supply choices than ever, consumer loyalty became fickle. As a result, the guarantee of emerging market growth has dimmed as tastes and options grew, disrupting distribution channels. As a result, grassroots brands figured out inexpensive ways to connect with consumers directly. These “upstart brands” had enormous success, eroding the share of traditional CPG powerhouses. According to BCG, between 2012 and 2017, small CPG companies grabbed about $15 billion in sales from their larger counterparts. (My favorite example is the beer industry, where craft breweries pop up constantly in local markets, eroding the market share of Miller Coors, Anheuser Busch, etc.)

Not only have sales been impacted but to quote the article: “Economic profit growth has nosedived. From 2000 to 2009, economic profit grew 10.4 percent per year; from 2010 to 2019, it dropped to 3.2 percent per year.”

In other words, brand erosion is driving major profitability concerns for most brands.

The central problem is that large brands no longer have a path to create unit growth. A closer look at the US market before COVID-19 is revealing. From 2017 to 2019, large brands (more than $750 million in revenue) in the US lost volume at the rate of 1.5 percent a year. At the same time, small brands grew 1.7 percent, and private label grew 4.3 percent.

If you’re interested in reading the whole article, which I recommend if you have the time, it elaborates on the trends impacting each of the five traditional playbook strategies and outlines ways CPG brands can win once again. There was a particular emphasis on the front-end channel, the consumer brand-building approach, and how to change it.

As most of our blog readers are focused on the supply chain, we will focus on the operational/supply chain recommendation:

How to Win Principle -> Evolving the operating model to excel at local consumer closeness and ever-greater productivity.

For most of us, this sounds like a pipe dream. Excelling locally while also driving greater productivity out of the supply chain?! What a joke, right? Getting closer means more local, last-mile infrastructure, more product touches, higher costs, and more SKUs. It can all feel a bit hopeless. But, when you dig in, you find that some players ARE not only delivering on this vision, it will be a continual focus point. Here are a few next steps:

- Start with the front-end of the business, rethinking your channel strategies, your marketing approaches, etc. If you’ve already done that and are seeing some success, push forward.

- Focus on digitizing and S&OP. You need to have strong demand sensing, as well as a fulfillment approach that works.

- Outsource all the non-strategic pieces you can afford. To do that, figure out what is non-strategic in priority order. Then, get non-value-add components off your plate and into a focused provider’s hand. We talk more about this here.

As always, focus matters. If you are a large brand incumbent, your front-end needs your best leaders’ focus, so outsource as much else as possible, without outsourcing the customer experience or end to end supply data.

We are going to tackle this topic further in future articles, so, if you haven’t already, be sure to sign up for updates from the Engineering Uptime blog!